Burning Inferno.

Your Bi-weekly update on edible oils & fats by Aveno

July 29th 2022.

Will the gasfather keep the lights on?

Undeniably the gasfather Vlad. Putin has his EU customers in a squeeze. Threatening to or really cutting off gas supplies drives up prices of all energy sources as people scramble for alternatives and take measures to mitigate risk from gas shortages.Already major industrial gas users are cutting production because it is too expensive to keep producing e.g., fertilizers and other basic chemical feedstocks. Higher energy prices thus also drive-up production, processing and logistics costs of edible oils and fats.

What is understood but often a forgotten obviousness is that the processing of oilseeds and refining crude oils requires a lot of energy like sweat, steam and electricity.

In the past, boilers ran on cheap heavy fuel and electricity came from the grid. But over the years this was replaced by gas, in order to meet stricter emission standards and reduce CO2 emissions. Today most modern energy efficient plants run on gas and have combined heat and power generation (CHP = WKK), meaning they also need the gas for electricity.

Probably gas will be more expensive in winter time but who can predict the price? And who can guarantee a steady supply of gas to the industry, power plants and homes? If the kitchen runs out of gas cooking stops. If power plants run out of gas the lights go out. Needless to say, price and risk are transferred to the customers in the price of edible refined oils and fats. But there is also a risk for the sellers if their buyers run out of steam, gas or money. Hope for the best prepare for the worst.

Burning inferno.

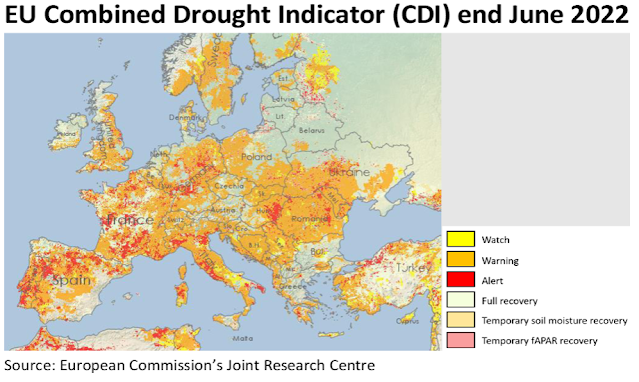

Europe’s been suffering from drought, heat and forest fires as severe drought in several regions of Europe since the beginning of the year expanded and worsened. In case of such events, EU’s Joint Research Centre reports on the situation and their latest report shows that some 46% of EU is currently in drought warning phase and 11% in the alarm phase. Crop yields in many countries are likely to decline by dry soils and vegetation heat stress.The European Drought Observatory uses a combined drought indicator (CDI) to identify areas hit by agricultural drought by combining a precipitation index, a soil moisture anomaly index, solar radiation absorbed by leaves, etc.

Lack of rain and heat waves impacted river water levels widely across Europe and impacted both hydropower generation and cooling systems of other power plants; reduced crop yield and crop yield potential as well as water storage volumes. Water supplies may be compromised in the coming months.

MARKETS

On paper the prospects for global oilseed and edible oil production in the 22/23 season still look promising and continued to exercise price pressure. In the field things look a bit different and weather scares will only vanish once crops are in store. Firmer energy prices supported edible oils & fats prices as well.An increasingly important swing factor is China with about 250 million people under covid-restrictions due to the zero-tolerance policy. This severely impacts the economy and after years of soaring real estate prices, China’s property bubble busted and there are concerns about the shakiness of China’s financial system. In the period oct 21 – June 22 vegetable oil imports dropped 50% vs the same period earlier. A pinch of salt though: China’s own oil production also increased because of the increased soybean crush for meal for their recovering hog industry. But still a huge number.

Olive oil

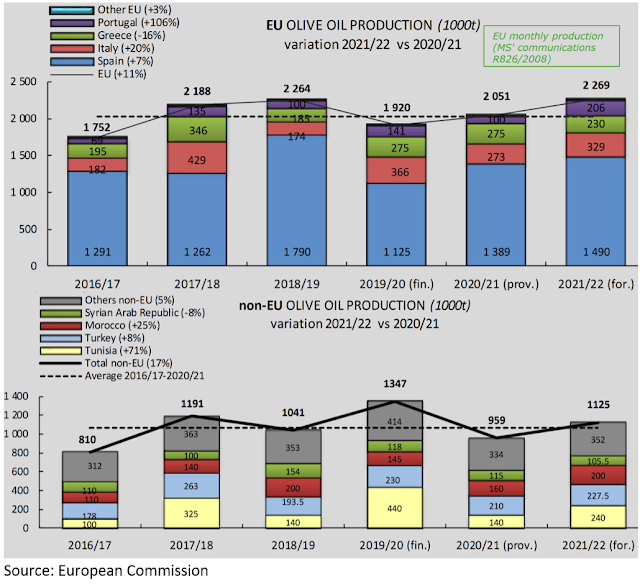

Unlike other edible oils, the price of olive oil is on the rise. There are major concerns as the ongoing drought and heat negatively impacts the development of fruits in the Italian and Spanish growing regions. Growers already see olive trees producing no fruit due to extremely low soil moisture levels. Unless it rains very soon, the olive crop will be dramatically reduced, likely causing further price increases. In producing countries, prices rose significantly above the past 5-year average. Some analysts forecast the Italian production of olive oil between 20% and 30% lower than last year and Spain might lose 15%.And then there is Xylella, the olive tree killing bacteria spread by insects. Xylella devastated most of the olive trees in the Salento region of Puglia and continues its devastating journey into EU. Xylella stops olive oil production, and shuts down olive mills, kills the revenues, employment, the traditions of generations and kills century-old trees. The bacterium of Latin American origin is also harmful to other plants and is moving up north. Fire and protective buffers are the only cure.

Spain is the largest olive oil producer and Italy annually imports between 450-475.000 mt of which about 300.000 from Spain. Much exported bottled olive oil from Italy has a Spanish passport.

On average, the global annual production of olive oil is 3Mmt of which about 2Mmt are produced in EU. Main producers are:

Support is found from stronger soybean oil prices; stronger mineral oil prices; and being the cheapest of all oils. China bought some oil and announced to import more palm oil from Indonesia (1Mmt) although this is not necessarily bullish news because if they need to buy palm olein because they crush less beans, this leaves beans to be crushed elsewhere. With forecasted strong meat prices everywhere, the crush will be meal driven making oil the weaker leg.

More dangerous support would come from higher gasoil prices which make palm oil biodiesel more attractive.

The sunflower oil market contemplates cautiously how the export deal, set up by the Turks between the Russians and Ukrainians, will evolve in practice. Also questioning the practicalities of the UA harvest (storage, transport, etc.).

Since the beginning of the war, oil consumption went down in Asia. Exports by boat to China, India, Iraq… dropped significantly and more went to EU by alternative routes. This allowed EU to build stocks of seeds and oil. If the flow goes on this will continue to pressure prices.

Mineral oil prices jumped over $100 again as traders stay under tension between fears of economic recession knocking down demand and increasing concerns about tightening European gas supplies after Russia cut the gas supply. Dwindling supplies of gas make it impossible for EU to replenish gas reserves ahead of winter. And there is talk of rationing gas… what will be the impact on all actors in the European food chain?

- Spain (66% of EU production);

- Italy (15%);

- Greece (13%); and

- Portugal (5%).

Corn oil

In the U.S., on top of inedible distillers’ oil from the biofuel ethanol production, more edible corn oil is used for biodiesel production. This leaves less corn oil for export and Spain already stepped out of the game. Spain used to import and refine and pack corn oil for export to northern African countries and the middle east. Of course, high prices didn’t help the business. Now in EU we also have a large processor of corn switch to wheat, by the end of this year, for the production of starches and glucose; meaning there will be no more corn oil from this plant. Corn oil is a by-product of wet-milling where corn germs are separated and crushed for oil.Soybean oil

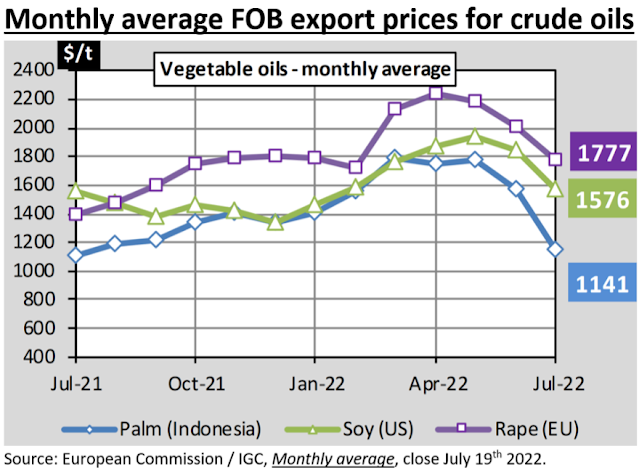

The entire soy complex is on an upward trend as heat is eroding confidence in a good crop. Especially the Mid-West of the U.S. is hot and dry and the forecasted hot and dry weather for August could limit yields as beans enter into a crucial development phase. The enormous gas and energy price increases support prices and in EU crushers and refiners will pass on this significant processing cost increase to their customers.Rapeseed oil

We saw firmer prices following a stronger Chicago soy complex, firmer petroleum prices and old crop tightness. In EU harvest is going forward with higher-than-expected yields, especially in Germany, but low water levels on the Rhine complicate logistics to supply crush plants. Rhine barges are currently loading only 50%, which means extra transport cost and hassle. Those who can work with railcars are luckier. These extra costs along with the enormous gas and energy prices, will be passed on by the rapeseed crushers and rapeseed oil refiners to their customers. The market hopes for better supply conditions in a fortnight. The rapeseed crop was made before the heat wave and harvesting 18.5Mmt would be 1.1Mmt more than last year. So new crop fundamentals could create some selling pressure when the supply tightness eases. In Canada confidence stays high for a good crop to be harvested September onwards.Palm oil

Palm oil prices moves nervously down and up on changes in the Indonesia policies. High stocks forced Indonesian palm oil mills to stop buying palm fruits which then rot on the plantation so authorities abolished the domestic sales obligation, they toy with B35 and B40 biodiesel ideas, removed temporarily export taxes till end of August… all measures to reduce burdensome stocks. But distress selling and flooding the market didn’t make the prices dive deeper and futures hover around 4000 ringgit/mt.Support is found from stronger soybean oil prices; stronger mineral oil prices; and being the cheapest of all oils. China bought some oil and announced to import more palm oil from Indonesia (1Mmt) although this is not necessarily bullish news because if they need to buy palm olein because they crush less beans, this leaves beans to be crushed elsewhere. With forecasted strong meat prices everywhere, the crush will be meal driven making oil the weaker leg.

More dangerous support would come from higher gasoil prices which make palm oil biodiesel more attractive.

Sunflower seed oil

In EU the sunflower seed crop suffered from dryness and heat and is revised down. Russia and Ukraine look OK weatherwise. Sunflower crushers in the east are less gas dependent as most produce their steam by burning the sunflower husks. But in NW EU that is, to doctor Aveno’s knowledge, not the case. But refiners of crude sun oil will also undergo the high energy prices and the risk of being cut off.The sunflower oil market contemplates cautiously how the export deal, set up by the Turks between the Russians and Ukrainians, will evolve in practice. Also questioning the practicalities of the UA harvest (storage, transport, etc.).

Since the beginning of the war, oil consumption went down in Asia. Exports by boat to China, India, Iraq… dropped significantly and more went to EU by alternative routes. This allowed EU to build stocks of seeds and oil. If the flow goes on this will continue to pressure prices.

USD, mineral oil and biofuels.

§§§

For questions or queries, please reach out to

AVENO

Aveno's Monthly OILS & FATS bulletins:

All our monthly bulletins: https://www.aveno.be/search/label/monthly

Don't forget to check out our bi-weekly updates!

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats. You can find all previous updates on: https://www.aveno.be/search/label/bi-weekly

Sign-up for Aveno's newsletters:

Disclaimer

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.