Oils & Fats, Economics and Politics.

Your Bi-weekly update on edible oils & fats by Aveno

September 14th 2022.

Petroleum is one of many commodities that loses buyers on a sad economic outlook and edible oils prices were pressured by the many bearish factors gaining more weight. The good outlook for rape and sunflower seed production on top of palm oil weakness kept a lid on prices. The Argentinian government came up with a new policy, the “soybean dollar scheme” which seems to be working, to encourage farmers to export more soybeans! And the Indonesian government actively continues to promote the export of palm oil to get rid of burdensome inventory. While Ukraine has been above expectations in finding alternative export routes (trucks, barges) and after the export deal with Russia many seagoing vessels loaded in UA ports.

A potentially deep economic recession and ample supplies remain a limiting factor for price increases. But as always there are two sides to every story.

Our Russian friend Gas Putin wants to revisit the deal on the Ukraine export corridor because “exports are going to the "West" and not to developing countries” and thus Putin wants to limit the deal to a number of selected countries. This created nervousness and supported prices a bit but so far everything goes as planned.

In the U.S. soybean oil has found support from the silently growing production of HVO (hydro treated vegetable oils as biofuel) despite the lower consumption of classic biodiesel (FAME or SME soy methyl esters). In Argentina the biodiesel admixture is back at 12.5% while Brazil and Indonesia are increasing their biodiesel usage too.

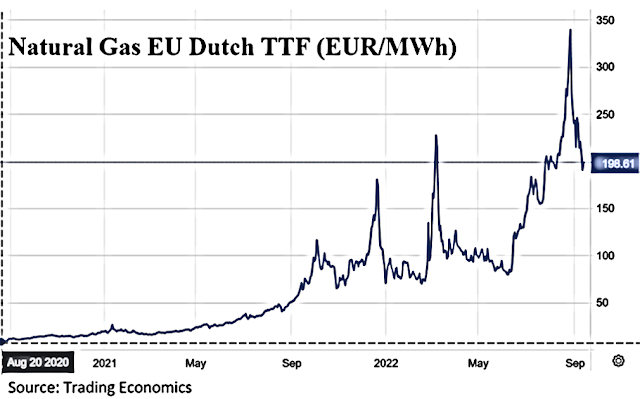

In EU oilseed prices came down but the very high energy prices lead to higher processing costs for crushers and refiners keeping prices of refined oils more than very well supported. And a weakening € increased the price of all $ commodities by more than 20% compared to two years ago. The euro may weaken further.

This week began with a rebound in edible oil prices following a bullish USDA/WASDE report on Monday.

It may also be that we get a softer economic landing than expected.

MARKETS

Soybean oil

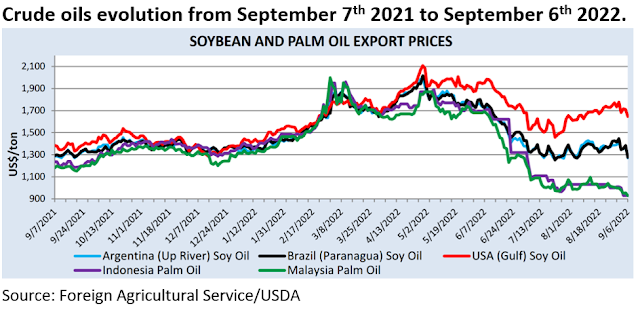

Since beginning September, the trend for the soy complex was down, mainly due to expected record sowings in South America and an expected record yield next spring. In addition, demand from China, the biggest bean buyer in the world, also decreased in 2022.Towards the end of the old crop season the oil leg in the complex found support from U.S. domestic demand for biodiesel production and from the reduced soybean crush in Argentina, the world’s largest soybean oil exporter. But everyone stayed optimistic on the new U.S. crop now being harvested.

The last WASDE report came a bit as a shock because since last month the USDA reduced its U.S. soybean production estimate from 123.30 to 119.15Mmt due to perceived lower yields. We shall recount the beans when they are all harvested and see what comes out of it. It will be key to watch the evolution of ending stocks in the U.S. and in the world which will be mostly influenced by south American weather, Chinese demand (revised down to 97Mmt) and north American biodiesel production and demand.

In Argentina, a new exchange rate arrangement was made between government and farmers, which means that farmers finally can sell their soybeans and get an honest pay for their hard work instead of only peso’s. Beans are already leaving the country.

Sunflower seed oil

Since June, Black Sea crude sunflower seed oil prices lost more than 30%, mainly due to the resilience of the Black Sea people finding solutions to their production and logistic problems. Not by spreadsheet management but the old-fashioned way: by working hard and getting on the road. They have been so successful that they now have a problem in finding a home for the production, since most EU buyers are more or less covered till the end of this year. It is expected that India and China will step in, to replenish stocks, to buy bulk oil as long as port loadings are possible.Ukraine’s sunflower seed production is revised up by 1Mmt to 10.5Mmt due to beneficial rainfall in August and Russia’s bumper harvest has just begun. The Russian crop will bring more seed and oil on the market which may pressure prices further.

Rapeseed oil

The availability of seed, meal and oil improved but the low water on some waterways is still a handicap to supply all crushers with seed. Rapeseed production in Australia was revised up again on recent beneficial rainfall improving yield prospects.Palm oil

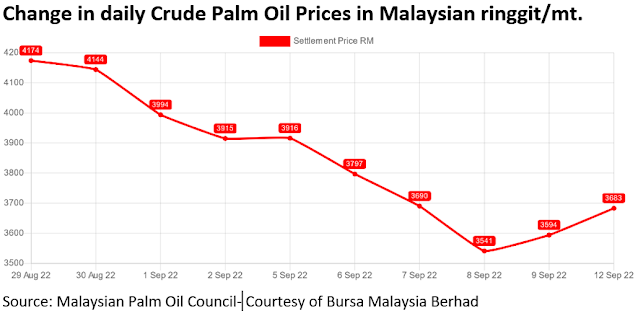

Palm oil prices continued to slip due to the Indonesian export policy and growing stocks. But since end last week palm oil prices rebounded on sympathy with stronger soybean oil and because it is still very attractive compared to alternative oils.

USD, mineral oil and biofuels

Though U.S. inflation is down to 8.3% YoY, but still higher than hoped, this strong number keeps the Fed on a hawkish path and supports the expected 75bp rate hike decision for next week.

Last week the ECB finally raised interest rates by 75 bps and the Euro recovered from slightly under to slightly above parity vs, the USD. But with the present interest differential between US/EU some expect the EURO to slip further down south.

Last week the ECB finally raised interest rates by 75 bps and the Euro recovered from slightly under to slightly above parity vs, the USD. But with the present interest differential between US/EU some expect the EURO to slip further down south.

Petroleum is struggling to stay in the $90-$100 range. Prices increased when the “Iran nuclear deal” talks appeared to go nowhere, which would keep Iranian oil off the market. Last week, an announced supply cut by OPEC+ wasoffset by a faltering Chinese economy. Demand from the world's biggest petroleum importer could even shrink this year for the first time in 20 years. The zero COVID policy keeps people off the street during holidays and reduces consumption.

§§§

For questions or queries, please reach out to

AVENO

Aveno's Monthly OILS & FATS bulletins:

All our monthly bulletins: https://www.aveno.be/search/label/monthly

Don't forget to check out our bi-weekly updates!

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats. You can find all previous updates on: https://www.aveno.be/search/label/bi-weekly

Sign-up for Aveno's newsletters:

Disclaimer

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.