Between fear and hope.

Your Bi-weekly update on edible oils & fats by Aveno

October 14th 2022.

Nervousness

After September ended as a bad month for financial markets, some optimism seemed to return early October when falling energy prices gave hope for less inflation. But hope got swept from the table by OPEC+ on October 5th after they announced a 2 million petroleum barrels production cut, saying that the shrinking Chinese economy was the main reasons for this decision.Generally, all markets remain rough with small waves, ups and downs and nervous about economic growth, inflation, central bank policies and growing concerns over a further escalation of the war in Ukraine.

Norway overtook Russia as Europe's largest gas supplier and gas flows from Russia via Ukraine have so far been stable, even though tensions in the region are rising. Gas prices dropped considerably from record levels seen earlier, helped by increased alternative gas supplies, mild temperatures and comfortable inventory (Germany 94.97% full and 98.97% in France). But storage levels account for only 23% of annual consumption….

What temperature should soup be served at?

Some analysts fear that due to different price caps and subsidies from EU governments, the savings of gas will be below expectations. And according to the International Energy Agency, shortages are still possible, so explosive price increases of gas and electricity cannot be ruled out. The most pessimistic fear winter blackouts with mobile telecommunications and internet going down, cutting us off from the rest of the world! But will the soup be eaten as hot at it is served? Only time will tell.MARKETS

Economic slowdown is already felt and affects global meat demand. Production of meat in several regions is down and it is possible that demand for ‘oilseed meal’ for animal feed will drop further and less crush will mean less oil production or more expensive oil to cover the processing costs. We also saw the demand for linseed oil curbed by the slowing economic activity just as large linseed crops (Kazakhstan, Russia, Canada) pressured prices of seed. But it is also interesting to see the second most produced oil in the world making a big premium vs. the most produced oil in the world: the spread crude soybean oil vs. palm oil is big. And GM-soybean oil is even more expensive than rape and sun.

Soybean oil

Wednesday the USDA released its monthly Global Agricultural Supply and Demand Estimates (WASDE) in which it, in line with expectations, revised up global soybean ending stocks:

In the U.S, soybeans have trouble getting from the production areas to the export terminals ‘down in Louisiana, where the alligators grow so mean’. Due to drought, the Mississippi water level is much lower than usual for this time of year which is causing delays and at a crucial point near Memphis, Tennessee the water is expected to drop even further. Meaning beans are piling up in the Midwest just as harvest is in full swing.

The Argentine government said farmers sold a record volume of more than 13.7Mmt soybeans in September, after the government allowed a more favorable exchange rate for producers.

Soybean oil prices remained firm because of good U.S. demand for biodiesel and because of less crushing in Argentina and EU where high energy prices do not favor crushing beans.

In Switzerland due to poor quality roughage and shortages, less milk for which the cheese and butter producers compete, was/is produced. At the request of the dairy industry, the Federal Bureau of Agriculture will, for the fifth time this year, increase the maximum quantity of butter that can be imported this year (totaling 13% of annual consumption).

- Global production was increased by 1.22Mmt to 390.9Mmt

- Ending stocks were increased by 1.6Mmt to 100.52Mmt

In the U.S, soybeans have trouble getting from the production areas to the export terminals ‘down in Louisiana, where the alligators grow so mean’. Due to drought, the Mississippi water level is much lower than usual for this time of year which is causing delays and at a crucial point near Memphis, Tennessee the water is expected to drop even further. Meaning beans are piling up in the Midwest just as harvest is in full swing.

The Argentine government said farmers sold a record volume of more than 13.7Mmt soybeans in September, after the government allowed a more favorable exchange rate for producers.

Soybean oil prices remained firm because of good U.S. demand for biodiesel and because of less crushing in Argentina and EU where high energy prices do not favor crushing beans.

Palm oil

Palm oil prices recovered some of the past losses on large exports from Indonesia and Malaysia, helped by the huge price discount vs. other oils and on sentiment coming from a bit firmer mineral oil price. But still Malaysian stocks rose to record levels.Olive oil

Prices strengthened further due to increasing expected production losses in Spain.Butter

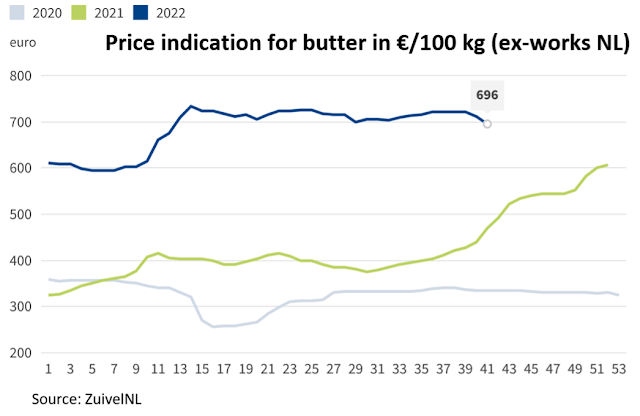

Average EU butter prices slipped slightly to € 7,203/mt mostly on lower prices in France and The Netherlands. Noteworthy is that in recent weeks American butter prices rose close to the EU butter prices. Underpinning that milk fat serves mainly the internal market for both EU and U.S. American butter stocks are at their lowest in 5 years and EU exports dropped (less export to China).In Switzerland due to poor quality roughage and shortages, less milk for which the cheese and butter producers compete, was/is produced. At the request of the dairy industry, the Federal Bureau of Agriculture will, for the fifth time this year, increase the maximum quantity of butter that can be imported this year (totaling 13% of annual consumption).

USD, mineral oil and biofuels.

The € slipped further after the Consumer Price Index (CPI) report, which measures the monthly price change for U.S. consumers (inflation), urged the U.S. Federal Reserve to continue raising interest rates, pushing the dollar higher. And so, pushing up imported inflation for other countries with low yielding currencies vs. the almighty dollar, the global reserve currency of choice. This forces central banks around the globe to also raise interest rates, risking a (deeper) recession for their economies.

Petroleum could not really rally and keep gains after the Opec+ announcement to cut production. Recession fears and lower demand forecast kept Brent near nearer to $90 than $100.

§§§

For questions or queries, please reach out to

AVENO

Aveno's Monthly OILS & FATS bulletins:

All our monthly bulletins: https://www.aveno.be/search/label/monthly

Don't forget to check out our bi-weekly updates!

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats. You can find all previous updates on: https://www.aveno.be/search/label/bi-weekly

Sign-up for Aveno's newsletters:

Disclaimer

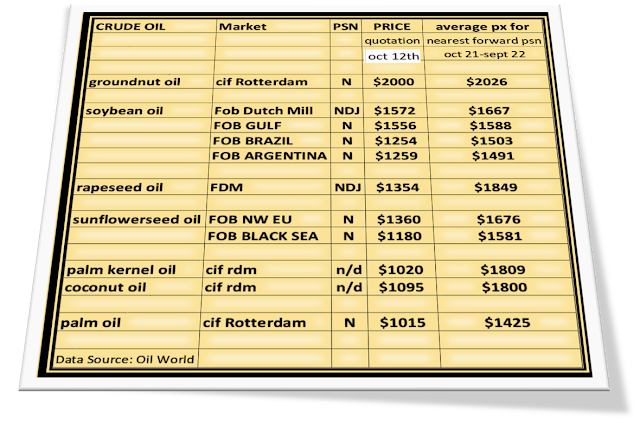

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.