Of darkness and light.

Your Bi-weekly update on edible oils & fats by Aveno

Late September a 3rd EFSCM (European Food Security Crisis preparedness and response Mechanism) meeting was held to assess the impact of the energy crisis on food security. The vital importance of energy for the continuity of domestic agri-food production was again underlined.

The cost and availability of fertilizer as well as energy consumption of animal feed plants, the monitoring of the cold chain (e.g., frozen meat and fries warehousing) and closer to home, struggling butcher shops and bakeries are all troubling topics of discussion.

Earlier in the month, FEDIOL (EU vegetable oil and protein meal industry association), had raised concerns about the cost and availability of energy needed for the production of vegetable oils. Implementing the 'Save Gas for Safe Winter' package (cutting gas consumption 15% next winter to save energy and reduce reliance on Russian gas) and disruption of energy supply worry food and feed businesses and may lead to serious food and animal feed shortages.

Higher oil and meal production costs come mainly from up to 12 times higher energy prices compared to the pre-war situation. Outside EU, energy costs "only doubled” and there is no CO2 tax, making the EU edible oils & fats sector and other food and feed players vulnerable and prone to more dependency on 3rd countries.

The USDA forecasted China to import 97Mmt soybeans in 2022-2023, the third highest amount ever. But as part of a broader plan to boost food security, the Ministry of Agriculture and Rural Affairs announced a reduction in the use of soybean meal in animal feed. For example, in 2021, the share of soybean meal in feed consumed by the domestic aquaculture industry fell 2.5% vs. 2017, saving 11Mmt of soybean meal = 14Mmt of soybeans.

China, the largest importer of soybeans and largest producer of soybean oil in the world, had increased soybean and soybean meal production in recent years. Crushing beans also means producing soybean oil. And if they don’t crush, they have to import (palm)oil.

On October 16th China will hold its 20th 5-yearly Party Congress to select the next party leadership and set the next five-year plan.

In EU crush margins for rape are better than for soy and bean crush requires more energy than soft seeds.

OPEC+ will sit together in Vienna on October 5th to discuss production cuts as to support petroleum prices. It can be that petroleum soars back to $100 and edible oil prices will rally on the news. We shall see and stay with the feet on the ground. Higher energy price won’t help revive the global economy.

The investments to produce HVO-biodiesel have been made and production is increasing. One outlet for HVO is SAF. The demand for animal fats and corn oil has become such that the U.S. turned from a net exporter to importer for these commodities. Soybean and rapeseed oil are in demand too.

The U.S. (60% of global corn oil production) reduced exports and increased imports just when production is stagnating and even decreasing because ethanol production (of which non-edible corn oil is a by-product) to replace gasoline is economically less attractive.

Animal fats are a byproduct of meat production which has been under pressure in the U.S. and EU. There’s been a sharp reduction in pork production in EU (DE, NL, BE, PL, FR…) which may never recover and cattle numbers too were down considerably in the U.S. and EU.

Today’s price premium of edible tallow FOB Gulf of Mexico of about $1000/mt over palm oil FOB Malaysia is not sustainable, but it remains a big concern for animal feed and oleochemicals as well as real ‘Belgian Fries’ producers who see their raw material supply go up in smoke!

Expect a tight global tallow and corn oil supply in 22/23!

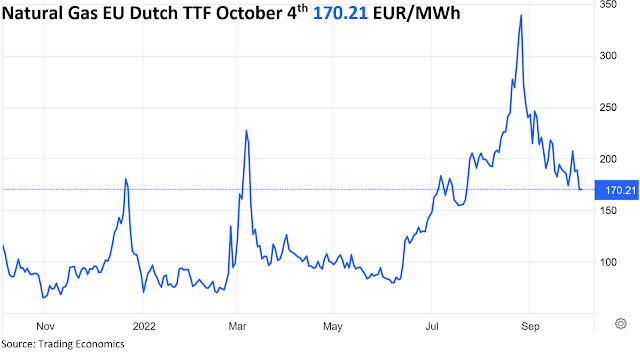

And as out-thrower the Dutch natural gas prices:

October 5th 2022.

The talk of the town

In all member states, food industry federations voice concerns over the survival of many of their members. Governments are urged to come with appropriate measures to mitigate the disastrous effects of high energy prices and to maintain a level playing field in Europe.Late September a 3rd EFSCM (European Food Security Crisis preparedness and response Mechanism) meeting was held to assess the impact of the energy crisis on food security. The vital importance of energy for the continuity of domestic agri-food production was again underlined.

The cost and availability of fertilizer as well as energy consumption of animal feed plants, the monitoring of the cold chain (e.g., frozen meat and fries warehousing) and closer to home, struggling butcher shops and bakeries are all troubling topics of discussion.

Earlier in the month, FEDIOL (EU vegetable oil and protein meal industry association), had raised concerns about the cost and availability of energy needed for the production of vegetable oils. Implementing the 'Save Gas for Safe Winter' package (cutting gas consumption 15% next winter to save energy and reduce reliance on Russian gas) and disruption of energy supply worry food and feed businesses and may lead to serious food and animal feed shortages.

Higher oil and meal production costs come mainly from up to 12 times higher energy prices compared to the pre-war situation. Outside EU, energy costs "only doubled” and there is no CO2 tax, making the EU edible oils & fats sector and other food and feed players vulnerable and prone to more dependency on 3rd countries.

The brightest stars

But every cloud has a silver lining. An economist pointed out that Germany’s gas consumption dropped 20% but industrial production receded only 2%. So far, a disaster was avoided and it shows the resilience of the industry. Steam generation for instance can also be done with mineral oil. Though there will be no or little ice skating on artificial ice this winter, more ‘rinks’ will open to roller skaters. The HORECA is suffering but resourceful: some open an hour later and compensate by closing an hour earlier. By doing so they save up to 25% energy. It is in the darkest skies that we see the brightest stars.MARKETS

Markets slid further but not yet back at levels of 2 years ago and the effect of raw material (oilseeds) prices for the production of vegetable oils and meals returning to pre-war levels in response to rising world production and stocks of oilseeds and oils (recovery of Ukrainian supplies, more ample availability of crops from EU, Canada and Australia and rising stocks of palm oil in origins) is at risk of being completely wiped out by a weakening Euro and higher processing energy costs. At least for EU consumers. Meanwhile Europe benefits from rainfall that is favorable for autumn sowings. Conditions in South America, however, are rapidly deteriorating.On China and beans

A contributing factor to high prices in the last years has been Chinese imports of oils & fats. A contributing factor for the recent price decline was China importing less oils & fats. Presently China is coping with a very difficult economic outlook: a deepening real estate crisis, a debt bubble totaling maybe 300% of GDP, an unusual high level of capital flight, youth unemployment above 20 % and Covid-related lockdowns.The USDA forecasted China to import 97Mmt soybeans in 2022-2023, the third highest amount ever. But as part of a broader plan to boost food security, the Ministry of Agriculture and Rural Affairs announced a reduction in the use of soybean meal in animal feed. For example, in 2021, the share of soybean meal in feed consumed by the domestic aquaculture industry fell 2.5% vs. 2017, saving 11Mmt of soybean meal = 14Mmt of soybeans.

China, the largest importer of soybeans and largest producer of soybean oil in the world, had increased soybean and soybean meal production in recent years. Crushing beans also means producing soybean oil. And if they don’t crush, they have to import (palm)oil.

On October 16th China will hold its 20th 5-yearly Party Congress to select the next party leadership and set the next five-year plan.

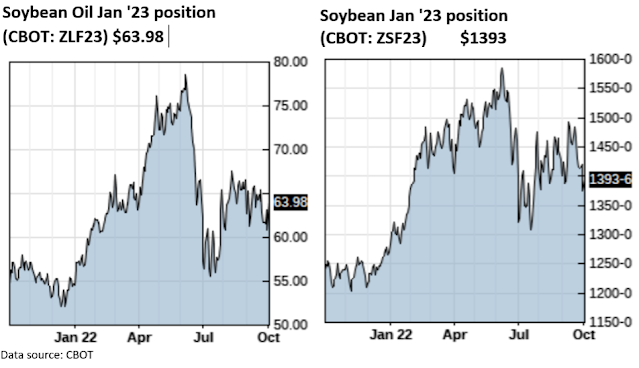

Soybean oil

Argentinian exports have pressured the market down somewhat. The delayed U.S. harvest is ongoing and should be round 22% complete by now but still a way to go. Last Friday the USDA reported higher stocks of soybeans than anticipated which pushed the three legs of the soy complex down. Farmer selling had been pushing bean prices down too. Brazil started its 2023 soybean crop sowings.In EU crush margins for rape are better than for soy and bean crush requires more energy than soft seeds.

Sunflower seed oil

After a five months blockade due to the war, Ukraine resumed exports from three black sea ports early August, as part of the Agreement, which took effect for a period of 120 days. Now Ukraine expressed doubts about the Black Sea export corridor after mid-November. Russian mobilization and escalation of the war increases the risk of Russia disrupting Ukrainian sea-going exports and that uncertainty is being priced in. The UA and Russian harvests have been delayed by rain. There is still a big stock of old crop sun seeds in EU as the imports from UA in the past months were big.Rapeseed oil

Price volatility remains. Crush and availability are good and on spot there is little demand so oil has to be discounted. Biodiesel demand seems to be picking up and the weaker Euro makes it interesting to export crude rapeseed oil. China has been sniffing around. Like the U.S., Canada is coping with a delayed harvest.Palm oil

Palm oil futures fell to their lowest in nearly 20 months on mounting fears about a global recession-driven demand destruction. Indonesia said it will keep the Domestic Market Obligation (DMO) policy alive (producers to supply the home market before exports) but had to push exports because tanks were overflowing due to a lack of storage capacity. So, despite the market bouncing up now and then, on exciting outside news, concerns about oversupply may limit upside potential. Some see futures dive to MYR 2,500/mt by the end of the year. But the future ‘s not ours to see. What will be, will be.USD, mineral oil and biofuels.

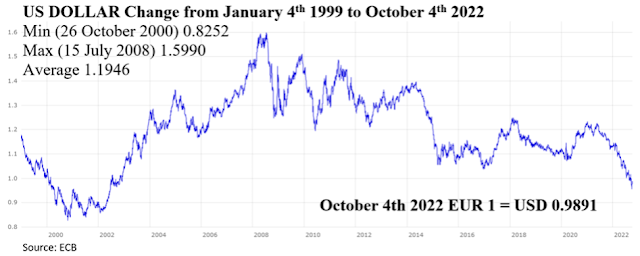

The Euro continued to weaken as USD is safe haven in uncertain war times, supported by higher interest rates and a stronger economy.OPEC+ will sit together in Vienna on October 5th to discuss production cuts as to support petroleum prices. It can be that petroleum soars back to $100 and edible oil prices will rally on the news. We shall see and stay with the feet on the ground. Higher energy price won’t help revive the global economy.

Something to watch.

Biden’s Inflation Reduction Act of August 16th, the single largest investment in climate and energy in American history, not only extends the existing biodiesel and renewable diesel tax credits but introduces a higher tax credit for sustainable aviation fuel (SAF). It is expected this will lead to more SAF production and there are concerns that the higher tax credits for SAF could divert sustainable feedstocks (like used cooking oil and animal fats), from other markets….The investments to produce HVO-biodiesel have been made and production is increasing. One outlet for HVO is SAF. The demand for animal fats and corn oil has become such that the U.S. turned from a net exporter to importer for these commodities. Soybean and rapeseed oil are in demand too.

The U.S. (60% of global corn oil production) reduced exports and increased imports just when production is stagnating and even decreasing because ethanol production (of which non-edible corn oil is a by-product) to replace gasoline is economically less attractive.

Animal fats are a byproduct of meat production which has been under pressure in the U.S. and EU. There’s been a sharp reduction in pork production in EU (DE, NL, BE, PL, FR…) which may never recover and cattle numbers too were down considerably in the U.S. and EU.

Today’s price premium of edible tallow FOB Gulf of Mexico of about $1000/mt over palm oil FOB Malaysia is not sustainable, but it remains a big concern for animal feed and oleochemicals as well as real ‘Belgian Fries’ producers who see their raw material supply go up in smoke!

Expect a tight global tallow and corn oil supply in 22/23!

And as out-thrower the Dutch natural gas prices:

§§§

For questions or queries, please reach out to

AVENO

Aveno's Monthly OILS & FATS bulletins:

All our monthly bulletins: https://www.aveno.be/search/label/monthly

Don't forget to check out our bi-weekly updates!

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats. You can find all previous updates on: https://www.aveno.be/search/label/bi-weekly

Sign-up for Aveno's newsletters:

Disclaimer

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.