Rambling on

Your Bi-weekly update on edible oils & fats by Aveno

December 2nd 2022.

Market participants had other things on their mind like the Eurotier Fair 15-18 November in Hannover, the HORECA Expo 20-24 November in Gent, the annual Grofor (Deutsche Verband des Großhandels mit Ölen, Fetten und Ölrohstoffen) dinner in Hamburg and Thanksgiving on the 24th, followed by Black Friday, the special public holiday in Malaysia on the 28th, the annual FOSFA oils and fats dinner in London on December 1st … and the market rambled on.

Volatility came from some nervous flash fire reactions to any scrap of news on China, the war, petroleum prices, the weather. After all, all it takes is one really bad crop somewhere in the world to send prices higher.

More fundamentally policy driven demand (biofuel policies), China’s economy, and depth of eventual global recession are the most important drivers. There’s been a lot of speculation or hope whether China would or wouldn’t ease it’s zero-covid policy following the civil unrest in the country, but that remains speculaas.

December 2nd 2022.

Unchanged story

After the COP 27 meeting in Egypt, mid-November the world’s population reached 8 billion people but that did not impact prices yet, neither in Kuala Lumpur nor in Chicago or on the MATIF. Maybe later, when the news sinks in.Market participants had other things on their mind like the Eurotier Fair 15-18 November in Hannover, the HORECA Expo 20-24 November in Gent, the annual Grofor (Deutsche Verband des Großhandels mit Ölen, Fetten und Ölrohstoffen) dinner in Hamburg and Thanksgiving on the 24th, followed by Black Friday, the special public holiday in Malaysia on the 28th, the annual FOSFA oils and fats dinner in London on December 1st … and the market rambled on.

Volatility came from some nervous flash fire reactions to any scrap of news on China, the war, petroleum prices, the weather. After all, all it takes is one really bad crop somewhere in the world to send prices higher.

More fundamentally policy driven demand (biofuel policies), China’s economy, and depth of eventual global recession are the most important drivers. There’s been a lot of speculation or hope whether China would or wouldn’t ease it’s zero-covid policy following the civil unrest in the country, but that remains speculaas.

MARKETS

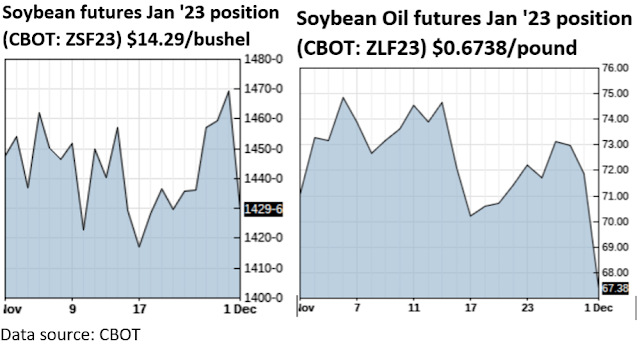

Soybean oil

In the U.S., the Environmental Protection Agency (EPA) proposed on November 30th to increase the quantities of ethanol, biodiesel and other biofuels that petroleum refiners must blend in their fuel. But the proposed annual increases of the blending obligations for 2023-24-25 were below market expectations and led to a sell-off of soybean oil futures. Under the Renewable Fuels Standard (RFS), petroleum refiners have to blend biofuels or purchase tradable credits (RIN - Renewable Identification Number) from those who do. The U.S. is exporting less soybean oil and its domestic consumption is up as well as biodiesel imports.

Dry weather in Argentina delayed soybean plantings and it’s also been drier than normal in Paraguay and southern Brazil. Meanwhile the region received a good amount of rain, easing the drought problem. An expected weakening of La Niña weighed on the market. A weather risk premium is still priced in and weather will continue to determine direction.

Brazil has less weather worries and plantings are near 80% done. There, the authorities said the biodiesel blending obligation will remain at 10% until March 31st. April onwards, it will increase to 15%. However, the next Brazilian government of President-elect Luiz Inacio Lula da Silva, taking office in January, could still change that. About 70% of the country's biodiesel is produced from soybean oil and a 15% mandate would push total soybean demand for biodiesel to 30Mmt in 2023. Discussions are also on whether or not to allow blending crude soybean oil with crude petroleum to co-process it to diesel fuel (95%/5%). The mandate could keep the market tight through the 1stquarter!

In EU, TTF natural gas went higher, increasing the variable crushing costs. Nevertheless EU-27 is processing beans and producing SME (soy methyl esters) which are exported to the U.S. of A! where demand for soybean oil and biodiesel is high. The blending obligation in the U.S. can also be fulfilled with imported biodiesel. There is no or little expensive soybean oil, which no one can pay, on the market. The soybean meal remains in EU for animal feed.

Brazil has less weather worries and plantings are near 80% done. There, the authorities said the biodiesel blending obligation will remain at 10% until March 31st. April onwards, it will increase to 15%. However, the next Brazilian government of President-elect Luiz Inacio Lula da Silva, taking office in January, could still change that. About 70% of the country's biodiesel is produced from soybean oil and a 15% mandate would push total soybean demand for biodiesel to 30Mmt in 2023. Discussions are also on whether or not to allow blending crude soybean oil with crude petroleum to co-process it to diesel fuel (95%/5%). The mandate could keep the market tight through the 1stquarter!

In EU, TTF natural gas went higher, increasing the variable crushing costs. Nevertheless EU-27 is processing beans and producing SME (soy methyl esters) which are exported to the U.S. of A! where demand for soybean oil and biodiesel is high. The blending obligation in the U.S. can also be fulfilled with imported biodiesel. There is no or little expensive soybean oil, which no one can pay, on the market. The soybean meal remains in EU for animal feed.

Palm oil

Production has peaked and exports from producing countries picked up. Productions were hampered by labor shortages and heavy rains. All this leads to a normal stock reduction and consequently supported prices. When petroleum and/or soybean oil goes up, so does palm oil, on rumors of China easing Covid restrictions, too. But we’re far from a price explosion. Production will go down till march to pick up again just as the South American crop hits the market!

Rapeseed oil

In EU rapeseed prices struggle not to fall in the dieperik. As there is more than enough seed for everybody, crushing is good and demand for oil is somewhat weak. The food market is mostly covered and buyers don’t want to chase the market higher while sellers hope for prices to return to higher levels. But also demand from biodiesel producers is weaker. Ample supplies of rape oil prompted RME (rape methyl esters) producers in EU to produce and because EU has imported a lot of UCOME (used cooking oil ethyl esters) from China there are now burdensome biodiesel stocks weighing on biodiesel feedstocks, even bringing UCO (used cooking oil) prices down.Traditionally towards Christmas and into January- February, food demand drops because before Christmas all should be delivered to the retailers and the holiday season begins. In the festive season people drink and eat too much, then they have left overs in the fridge, they don’t eat much salads in winter and they have empty wallets. Appetite revives by mid-February on the feast day of the Italian Saint-Valentine, the patron saint of love.

Markets stay tricky though and as rapeseed oil is competitive against other liquid oils like soy and sun, one may expect an export revival. So, on weak European demand crushers and refiners could dump their production in the export market.

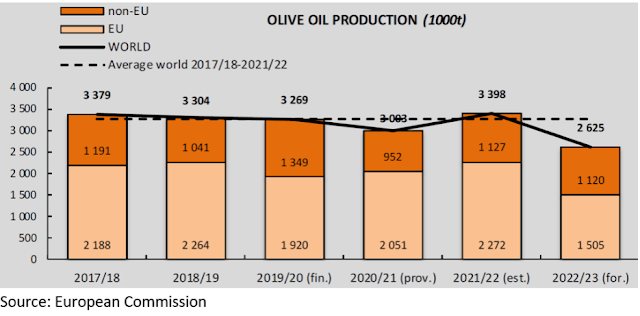

Olive oil

Olive oil prices continue to look for new highs following the drought related production reduction in the Med! The only country with an increased production is Turkey which could eventually put some oil in the export market to catch some of the high prices. But quantities are inferior to 200.000 mt and one needs to calculate with Turkish export duties and EU imports duties. For example, Portugal sees a 40% drop in olive production and Spain is not doing much better!

Sunflower seed oil

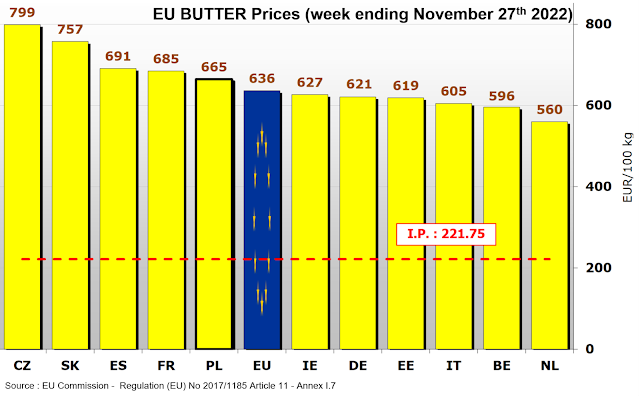

India and China have been buying oil and in EU there are still good stocks of seed and oil. Russia's continued artillery fire on Ukrainian power plants and infrastructure left half the country without electricity, making most export ports unusable, even on the Danube. This is something to monitor closely in the coming year. Ukrainians are resilient and resourceful and we hope for the war to stop soon.Butter

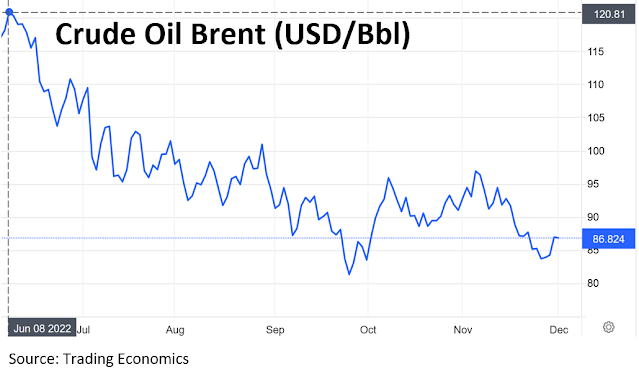

USD, mineral oil and biofuels.

Coming diesel/gasoil shortage?

Petroleum firmed somewhat on speculation that OPEC could decide to cut production, at its next meeting December 4th, to drive prices above $90 but weak Chinese demand is not helping. China remains the big bearish issue for the rest of the year as many expect China's zero COVID policy to remain in place until springtime next year. But no one really knows.

§§§

For questions or queries, please reach out to

AVENO

Aveno's Monthly OILS & FATS bulletins:

All our monthly bulletins: https://www.aveno.be/search/label/monthly

Don't forget to check out our bi-weekly updates!

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats. You can find all previous updates on: https://www.aveno.be/search/label/bi-weekly

Sign-up for Aveno's newsletters:

Sign up formDisclaimer

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.