It creaks and it squeaks.

Your Bi-weekly update on edible oils & fats by Aveno

Bi weekly June 12th 2023.

Bi weekly June 12th 2023.

Notwithstanding the world is round, it peeps and creaks in every nook and cranny.

Once again, a continuing weak global economic outlook was confirmed by falling petroleum prices when economic fears overshadowed Saudi Arabia’s announcement of petroleum output cuts in July.Although mild, the Eurozone was officially declared in recession and with the ongoing economic deterioration in the US,renewed doubts rose about interest rate increases. Inflation and ‘greenflation’ as well as public debt in US and EU remain major concerns and it is still unclear whether the delayed effect of monetary tightening to combat inflation will lead to a crash or not.

In China, Q1 post-covid effects of postponed orders have worn off and economic recovery is clearly failing.Contracting industrial production, lower consumption, the (real estate) debt problems and falling exports weigh heavily on the recovery of the second largest economy in the world. And next to multiple emerging stories on the ‘risk of deflation’, the geopolitical tensions around Taiwan lead some to invest less or leave China.

Finally, recent turmoil in EU with alleged fraudulent biodiesel imports, global re-questioning the feedstocks for the production of (advanced)biofuels, rising uncertainties around policy driven demand and jeopardized return on investments (made to satisfy policy driven demand) are leading to sleepless nights for many.

Yet the world continued turning smoothly, lubricated by an abundance of vegetable and animal oils and fats!

MARKETS

The two exceptions to abundance, confirming the rule, are fish and olive oils. Both oils face rationing of demand. In EU, olive consumption and exports were already reported about 10% lower. This is expected to happen to fish oil as well, rather sooner than later. Peru just cancelled its first anchovy fishing season, which began with a disappointing exploratory research trip on June 3rd. Things will be reassessed in 2-3 weeks. Depending on the size of the “core demand” what price the market can and is willing to pay, is anybody’s guess, but it won’t be cheap.Otherwise, markets remain in a wait and see mode, mostly inspired by an uncertain and often intangible economic context. Food demand in developed countries is, for a great part, mostly inelastic. The globally growing nonfood use of edible oils and fats have, if not being determinant, a bigger impact, on price formation than food use. Nonfood use is not only in energy but also in the chemical and other industries.

Generally vegetable oil prices dropped to levels not seen since end 2020 on ample supplies and weak demand and the million bucks’ question is if they will drift lower. The only reason to buy deferred, today, would be the sum of lesser crops such as Argentina beans, Australian rape, fish oil, olive oil, and weather scares for future crops due to El Nino, a premature gamble on the weather. With the wimps of weather price volatility may get extreme, though.

Animal fats

Some cracks are appearing in the sky is the limit story. Prices may collapse and it is risky being long animal fats these days. Prices of animal fats seem to be coming off the highs and moving in line with vegetable oils as the SAF (sustainable aviation fuel) industry is reducing its positions. Due to competition from the alleged illegal imports in EU of biodiesel from China, several factories shut down, meaning less domestic demand. Producers of animal fats are now sitting with the baked pears and tightening the belt. Those who saw this coming are bulking up in tanks for export to the US where demand and prices are still strong. Trade flows can adapt quickly and boldly go where no man has gone before.Soybean oil

We are a bit in a weather market and it looks like it will remain mostly dry for the foreseeable future, although some light showers were in the forecast for some parts of the US where soybeans prices tried moving higher, but struggle to keep gains. Soybean plantings are over 90% done versus an historical average of 75% and growing conditions look good to excellent in 65% of the acreage.Last Friday’s WASDE report left a bearish reminder that US bean supplies are growing as the market struggles with the huge Brazilian crop of 156Mmt, which undercuts US exports. This made the USDA raise both old crop and new crop ending stocks and cut a surprisingly large part of US soybean exports. But, we’re still early in the growing season and ahead of the big June Acreage Report.

Soybean oil has been supportive to beans in the US. The focus on oil demand giving soybeans a boost, kind of put a floor in the US bean market. Some end-user buying stepped in and funds went for short covering.

There is some disconnect with the rest of the world, because of the big crush expansion in the US, following the future growing demand for hydro treated vegetable oil or HVO as biodiesel/aviation fuel (with low carbon fuel subsidies). As the US becomes a net importer of all kinds of edible oils and fats to supply their biofuel industry, the market there might become a kind of global reference for the value of animal fats, UCO, soybean oil, etc. and create arbitrage opportunities (simultaneous purchase and sale of the same commodity in different markets to profit from unequal prices). Using other feedstocks for biodiesel might also pressure down prices of soy oil in the US but the right balance between production capacity, utilization rate and availability of feedstocks is still much evolving. A lot of unknowns yet and it is worth noting the price differences for crude soybean oil on June 1st:

- fob Gulf of Mexico $1165

- fob Dutch mill $900

- fob Brazil $874 ……………..vs crude palm of $795 fob Indo

Rapeseed oil

The return of El Niño, with below average rainfall in Australian agricultural regions in winter (until August) and spring (Sept-Nov), could lead to a significant drop in yields. ABARES, the Australian Bureau of Agricultural Economics and Science, estimated rapeseed production could drop 41% from last year’s record to only 4.9Mmt! This would still be 15 % above the 10-year average but would logically lead to a drop in exports in the 2023/24 marketing year. They also take into account farmers will not use the land most sensitive to dryness.Canada had scattered showers over major growing areas helping restore some soil moisture and more remains in the forecast. Meanwhile forest fires and heat remain a major threat.

In EU the seed carry out this year is at a 5-year high, heavy and adds to availability next season. Drier weather and price drops attracted some buying interest. In its latest update the European Commission raised its forecast to 20.2Mmt rapeseed in 2023/24, up from 20Mmt in April and 19.5Mmt last year.

Going forward weather and developments in Ukraine will continue to influence the market. Oil usage in EU stays below expectations mostly due to subdued biodiesel production.

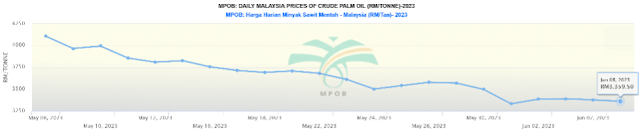

Palm oil

Production growth keeps slowing down due to aging trees and insufficient replanting. El Nino might, in the future, limit production. Palm is cheaper than Brazilian soy oil, which should attract more buying interest.

On the other hand, EU is phasing out gradually the use of palm oil as biodiesel feedstock; those are big numbers. And for the first time ever Malaysia and Indonesia joined forces to defend palm oil against the threat of anti-oil palm campaigners. Then, Indonesia's Coordinating Economic Affairs Minister voiced hopes that the UK won’t follow EUs recently issued “EU Deforestation-Free Regulation” (EUDR). And with the global economy in limbo the whole oleo-chemistry-industry is also not booming and waiting for better times to come. Hence also the big stocks of laurics in origin.

Sunflower seed oil

The May update of crop forecasts from the Commission kept EU sunflower seed production estimated at 10.5 million mt which is considerably higher than the 9Mmt seen last year and about 8% above the five-year average. Accumulation of stocks in Türkiye add to the heaviness. But situation in Ukraine keeps throwing in uncertainties which firms prices but availability remains ample.USD, mineral oil and biofuels.

Saudi Arabia, at an OPEC+ meeting a week ago, decided to unilaterally cut its petroleum output by 1Mbbl/day starting in July. The intention was to put a floor in the market through a broader agreement to limit supply until 2024. Last Friday, prices were back at pre-meeting levels as the economic outlook is too uncertain for prices to really recover. Speculating on a further deterioration of the global economy, ‘shorters’ pushed prices lower helped by a larger-than-expected increase in gasoline inventories in the US and weak Chinese economic data.

Biodiesel developments

Motivated by a desire to lower the cost of living for its citizens in a context of runaway inflation, Sweden's newly elected minority coalition cut fuel taxes, increased tax breaks for people who commute to work by car and ended subsidies for new EV’s. Under current Swedish law, diesel must contain 30.5% biofuel (increasing annually) and it was also decided to reduce that admixture to 6% in 2024 and to maintain that till the end of 2026. A lot of biodiesel made from animal fats and UCO is used. Now Finland would also question the use of animal fats and UCO for biodiesel and furthermore, according to a new study commissioned by 'Transport and Environment', the British government is also considering a strict limit on animal fats and used cooking oil use in the aviation industry, due to concerns about unintended consequences. The discussion there is more about the fact that diverting animal fats and UCOs from road transport fuels to sustainable jet fuel makes little sense.There has been protest from the petfood and the oleochemical industry against using one of their raw materials for biodiesel as they would have to replace animal fat by e.g., palm…. One way or another this will get solved, but by putting numbers, like kilos and euros, against this development, it can evolve into a completely new ball game.

And to make everybody cry: beginning this month EWABA, the European Waste-based & Advanced Biofuels Association, wrote a letter to the key decision-makers in the European biofuels sector, asking urgent intervention to save the European Waste-based and Advanced Biodiesel industry as “nearly half of EU waste-based and advanced biodiesel plants are currently halted or operating considerably below their normal production”. According to the letter 11 plants where completely down. This is allegedly due to unfair competition from China. Meanwhile Germany officially asked EU to look into the matter.

In EU, margins for biofuels are in the grave and optimism popped up once again when Total Energies announced last week, investments to double its SAF production at Grandpuits (near Paris), bringing the annual production capacity of “biofuels produced from waste and residues from the circular economy (animal fats, used cooking oils, etc.)” to 285,000 mt. Hope is always the last to die.

§§§

For questions or queries, please reach out to your regular AVENO contact

Don't forget to check out our previous bi-weekly updates!

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats.

You can find all previous updates here

Newsletter sign-up

Sign-up here to receive our Biweekly directly into your inbox.

Disclaimer

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.