Your Bi-weekly update on edible oils & fats by Aveno

Bi weekly October 2nd 2023.

Economic headwinds.

In EU, the chemical industry complains about high wage and energy costs that put in danger the viability of the industry which is running on only 70% of capacity on poor demand, from e.g., car manufacturers and construction companies. There is increased talk of restructuring, cost cutting, closures and even layoffs.

The problems in the Chinese real estate sector, good for 25 to 30% of GDP, and on the verge of collapse, will contribute to a slowdown in global economic growth. Problems with Evergrande, the world's most indebted developer, have been in the headlines for some time, but many other developers are also in financial trouble. Country Garden, China's largest property developer by revenue, narrowly avoided defaulting on a debt payment last month. The government hopes it can contain the fallout of bankruptcy and asked local governments, themselves heavily in debt, to prepare for the social and economic consequences of the official bankruptcy of Evergrande. Normal economic laws also apply in China, and the long praised economic technocrats will now have to ensure that the real estate and debt crisis doesn’t hurt the rest of the economy too much.

More often, on many occasions, the overall sentiment remains rather bearish due to economic headwinds affecting demand. To sum it up, in the last DG Agri MMO Economic Board meeting of Sept. 25th one of the conclusions, applicable to most markets, was the following:

“Confronted with inflation, consumers are actively searching for promotions and switching to less expensive food. Consumers are reducing their purchase of fresh products, organic food and premium products. Fewer consumers are willing to pay a higher price to get healthier products. Products with private labels are gaining market shares as well as discounters.”

MARKETS

Palm oil

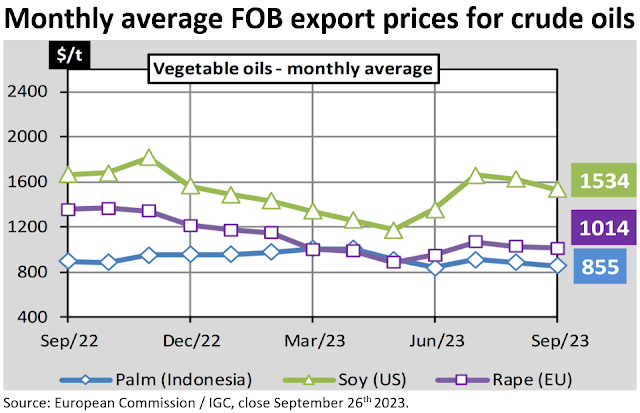

Palm oil mostly continues to move sideways. A bit up and a bit down. Palm stays impacted by spillover effect of other weakening oils on one hand and by higher petroleum prices on the other. In Kuala Lumpur, futures after moving down staged a recovery, driven by a recovery in Malaysian exports and the development of an unfavorable weather environment for plantation productivity. To watch are the evolution of stock building in origin and the use of palm oil in biodiesel in both Indonesia and Europe, despite palm oil bans in several member states.

Soybean oil

The USDA’s ‘quarterly inventory report’ from Friday, September 29th, was bearish for soybeans. Following the release, beans were down 19 cents and could suffer more price pressure as harvest progresses. The USDA lowered soybean production by 6M bushels but still ended up with a 268Mbushel carryout which is more robust than expected; ending stocks for 2022-23 were put at 250M bushels. The next WASDE report is due on October 12th.

Low water levels on the Mississippi continue to limit export capabilities and the cost of getting crops out of the Midwest is going to be higher and it will take much longer. Loading drafts and the number of barges a single tugboat can tow are restricted to lower than normal. A situation expected to remain till the end of the year.

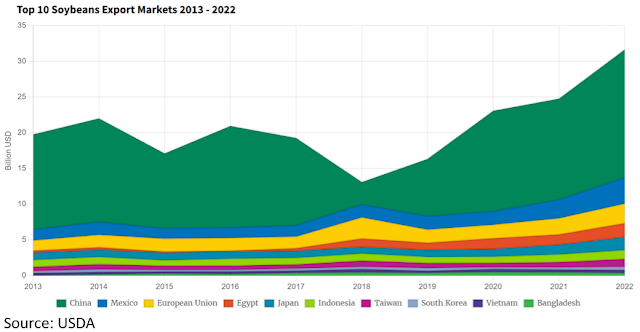

On the demand side for agricultural commodities, in general and including meat, increasing tensions with China will drive China to further diversify away from US dependency. The current economic headwinds in China are also a growing concern as it is a major (global)demand driver which can become a very strong negative.

The market’s focus now goes to South America where sowing started. Dry weather in Brazil and Argentina threatens timely plantings but it is too early to draw any conclusions.

Rapeseed oil

Rapeseed prices are balancing between the supply push of Ukrainian origin seed and the demand revival from the EU biodiesel industry as petroleum prices restored strength to the biofuel industry.Seed prices lost volatility since mid-September and stabilized around €445/mt on nearby while European imports remained limited. Globally the oilseed complex is under pressure due to the progress of the US soybean harvest and strong competition from Brazil. In Canada, the good rapeseed harvest progress pushed seed prices to their lowest level since late June, despite an expected significantly lower supply in 2023 than last year (17.5Mmt vs 18.69). Larger than foreseen crops in Ukraine and Russia compensate amply the lower Canadian and Australian production.

Big supplies and weakness in other oils (e.g., sun oil) weigh on the market.

Sunflower seed oil

The record Ukrainian seed production of 15Mmt vs. 12.3 last year and the 13.3Mmt in Russia, same as last year, continue to weigh heavily in the Black Sea market. Favorable weather helps accelerate harvest progress in key production regions although farmer selling has been slow.The oil markets are in a steep carry suggesting huge stocks to be carried and recent weakness in palm and soy oil kept overall pressure on prices.

Butter

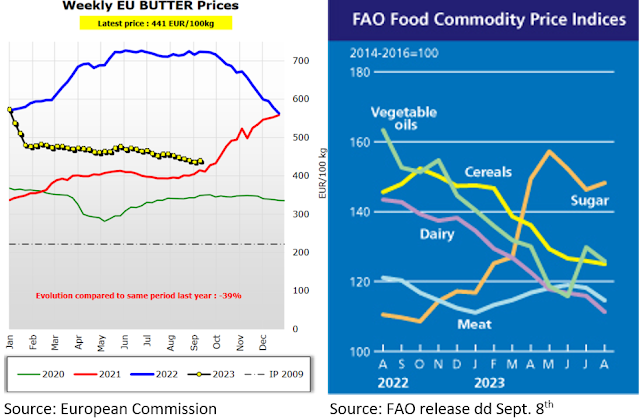

Cream (30-40% fat) prices gained in September on increased demand as the month progressed and sentiment got relatively upbeat. Butter (82%fat) prices followed the cream market and the firmed in the past weeks. Average European price would now be well above €446/100 kg. We saw prices in France at €472/100 kg, €464 in Belgium and €454 in the Netherlands; but that is still more than 30% below what they were a year ago. As stocks of butter are still high, a correction might well be sitting in the waiting room.

Olive oil

In Spain, normally good for nearly 50% of the global olive oil supply, carry out stocks are at an all-time low and some fear olive oil stocks could be exhausted before oil from the new harvest, which usually starts around October, hits the market. Having said that, it is very difficult to assess the real total olive oil stocks in Spain and a lot is uncertain. If the situation can worsen, remains to be seen, but next global olive oil production is expected to be well below normal. For Spain a forecast of merely 650,000 mt is far below a usual 1.3Mmt. Dryness and heat also affected Greece, Morocco and Italy. This year Greece, for example, is expected to produce a third less than last year or only 200,000 mt. Tunisia, Turkey and Syria announced a ban on olive oil exports to protect their domestic markets.USD, mineral oil and biofuels.

Economic headwinds in China could stop their strong imports and longer term as the post-pandemic recoveries will have run their course completely, and with the energy transition picking up pace, global demand may ease… But, more people on earth means more demand for energy.

Biodiesel developments

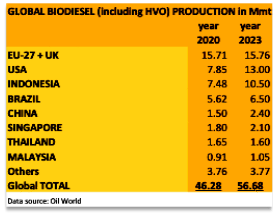

This year global biodiesel production is to grow from 52.07Mmt in 2022 to 56.68Mmt mainly on account of the US and Brazil. Used feedstocks are diverse and in EU 6.5Mmt of rapeseed oil is used for biodiesel production out of a total consumption of 9.7Mmt in 2022. Meaning that only about 3Mmt or one third of total consumption goes to food use.

§§§

For questions or queries, please reach out to your regular AVENO contact

§§§

Previous bi-weekly updates

There is some complexity to the business we daily operate in. To help understand the business of being an edible oil and fat producer we've launched a bi-weekly newsletter.

Every two weeks we will share an update about edible oils and fats.

You can find all previous updates here

Newsletter sign-up

Sign-up here to receive our Biweekly directly into your inbox.

Disclaimer

Unless otherwise mentioned the crude oil values quoted in these documents are prices landed in EU without import duties, handling, storage, financing, refining, packing, transport or any other cost related to bring the product to market. They are used as market trend illustration. Substitution of oils is possible but different oils have different fatty acid profiles and are not all interchangeable for all applications. One can make biodiesel from all oils and fats but one cannot make mayonnaise from coconut oil. This document is exclusively for you and does not carry any right of publication or disclosure. This document or any of its contents may not be distributed, reproduced, or used for any other purpose without the prior written consent of AVENO. The information reflects prevailing market conditions and our present judgement, which may be subject to change. It is based on public information and opinions which come from sources believed to be reliable; however, AVENO doesn’t guarantee the correctness or completeness. This document does not constitute an offer, invitation, or recommendation and may not be understood, as an advice. This document is one of a series of publications undertaken by AVENO and aims at informing broadly a targeted audience about the edible oils & fats market. AVENO’s goal is to keep this information timely and accurate however AVENO accepts no responsibility or liability whatsoever with regard to the given information.